TL;DR:

- Effective evaluation of cybersecurity hardware ventures requires technical benchmarks, IP verification, and understanding market moats to identify defensible companies. Investors should focus on threat detection accuracy, rapid incident response, and proprietary physical IP to avoid commoditization risks. Long development and sales cycles, along with on-premises market opportunities, make DPI and real-world customer validation crucial for success.

Cybersecurity hardware venture assessment is the structured process of evaluating hardware security startups through technical, market, and operational due diligence to determine investment viability. Entrepreneurs and investors who skip this process routinely overpay for compliance theater dressed as defensible technology. The global cybersecurity market is projected to exceed $300 billion by 2028 with a 13% CAGR through 2030, which means capital is flowing fast and the cost of a poor assessment compounds quickly. Palo Alto Networks, CrowdStrike, and Cisco have each absorbed promising hardware ventures that lacked the IP depth to survive as independent entities. This guide gives you the framework to tell the difference before you commit capital.

What key benchmarks define strong cybersecurity hardware ventures

The technical evaluation of a hardware security startup begins with quantitative thresholds, not pitch decks. Best-in-class threat detection exceeds 99% accuracy with a false positive rate below 0.1%. That second number matters as much as the first. High false positive rates generate alert fatigue, which causes security teams to ignore real threats and drives churn.

Incident response speed is the second critical benchmark. Top-performing hardware solutions achieve mean time to response under 24 hours. The industry average sits at 197 days, which means a startup claiming sub-24-hour response is not just better. It is operating in a different category entirely. Verify this claim with customer references, not internal dashboards.

Operational stickiness is measured through gross churn rate. Churn below 8% signals that customers treat the product as operationally necessary, not discretionary. Hardware solutions embedded in physical infrastructure tend to achieve this threshold more reliably than software-only alternatives because replacement costs are high.

Deployment speed also carries weight. Hardware solutions requiring more than 60 days to deploy risk losing customers mid-cycle when budget priorities shift. Short deployment cycles correlate directly with enterprise adoption and retention, particularly in regulated environments where procurement windows are narrow.

Key technical benchmarks to verify during initial screening:

-

Threat detection rate: Greater than 99% with false positives below 0.1%

-

Mean time to response: Under 24 hours, verified by third-party audit or customer reference

-

Gross churn rate: Below 8% across the active customer base

-

Deployment cycle: Under 60 days for full operational deployment

-

Bug bounty program: Active, public, and funded. Absence of a bug bounty program signals either untested security or fear of scrutiny. Both are disqualifying.

Pro Tip: Ask the founding team to walk you through their last three bug bounty submissions and how they were resolved. The specificity of their answer reveals more about security maturity than any certification document.

How to conduct technical and market due diligence for hardware ventures

Due diligence for hardware cybersecurity ventures follows a more demanding process than software-only investments because the attack surface includes physical components, firmware, and supply chain integrity. The sequence below reflects what institutional investors and CISOs expect to see before a term sheet is signed.

-

Request third-party penetration test reports dated within the last 12 months. Relying on internal security claims for hardware-based solutions introduces significant risk. Independent red team reports from firms like NCC Group or Bishop Fox carry weight. Internal claims do not.

-

Audit intellectual property ownership. Verify that core algorithms, cryptographic methods, and hardware designs are owned outright by the company, not licensed from a university or a prior employer. Patent filings, assignment agreements, and cryptographic audit reports from firms like Trail of Bits are the documents you need.

-

Validate the total addressable market with customer evidence. TAM figures in pitch decks are projections. Conversations with two or three CISOs who are active customers or serious prospects give you ground truth. Ask them whether they would replace the solution if a competitor offered a 20% discount.

-

Confirm compliance posture. SOC2 Type II certification is a baseline expectation in 2026, not a differentiator. Ventures without it face valuation discounts and extended sales cycles with enterprise buyers. Also verify alignment with GDPR, the EU AI Act, and the EU NIS2 Directive where applicable.

-

Screen for regulatory exposure. Export controls, FedRAMP authorization, and multi-state privacy laws each create distinct compliance timelines. Early identification of these obligations prevents costly delays after capital is deployed.

The following table summarizes the documentation required at each due diligence stage:

| Due diligence stage | Required documentation |

|---|---|

| Technical security | Third-party penetration test report (within 12 months), red team findings, bug bounty history |

| Intellectual property | Patent filings, IP assignment agreements, cryptographic audit reports |

| Market validation | CISO reference calls, signed LOIs or contracts, TAM analysis with named customer segments |

| Compliance | SOC2 Type II certificate, GDPR data processing agreements, FedRAMP authorization status |

| Regulatory risk | Export control classification, NIS2 compliance roadmap, multi-state privacy law assessment |

Red flags that warrant immediate scrutiny include founding teams with no prior hardware security experience, absence of any compliance certification, and architectures that depend entirely on third-party APIs for core security functions.

How to map competitive position and assess durable moats

Competitive analysis in cybersecurity hardware requires more precision than a standard market map. The relevant question is not who else operates in the space. The question is whether the startup solves a problem that Palo Alto Networks, CrowdStrike, or Cisco has structurally ignored or cannot address without cannibalizing their existing revenue.

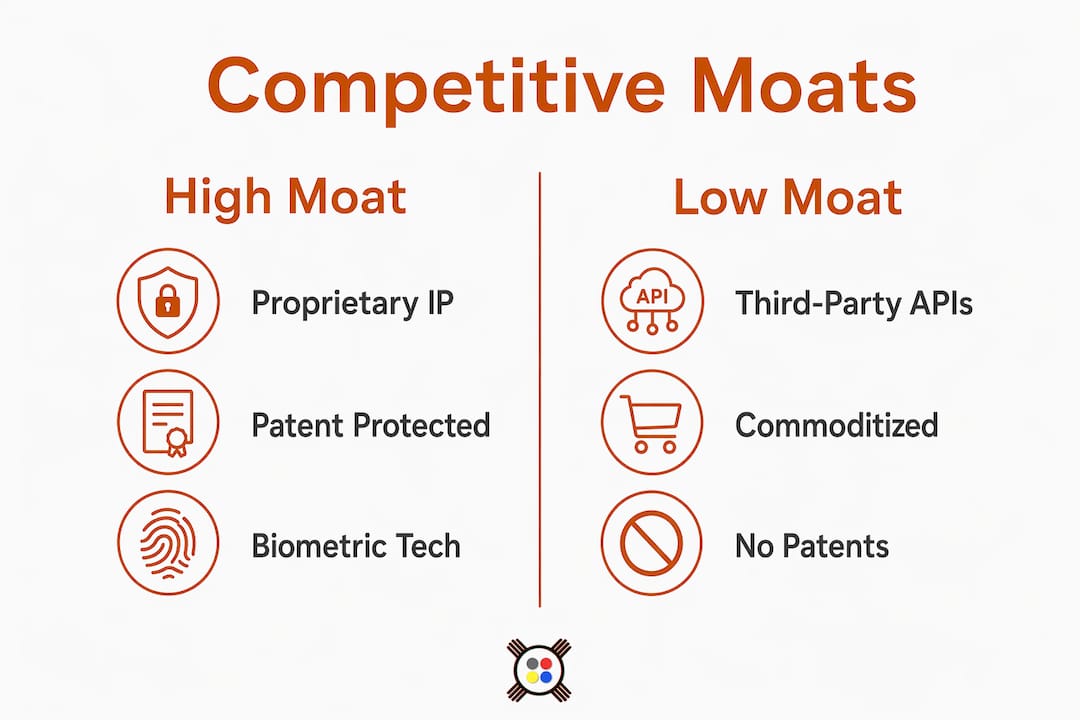

Solutions without proprietary intellectual property or those built primarily on third-party APIs face commoditization risk within a single product cycle. This is the “Sherlocked” problem. When a platform giant ships a native feature that replicates your product’s core function, a wrapper company has no defense. A company with proprietary cryptographic hardware, patented sensor arrays, or novel biometric authentication methods has a structural moat that cannot be replicated by a software update.

The table below distinguishes between defensible and commoditized positions:

| Venture type | Competitive moat | Acquisition risk |

|---|---|---|

| Proprietary hardware IP | High. Patent protection and physical integration costs create switching barriers | Low. Acquirers pay premiums for owned IP |

| API wrapper on third-party platform | None. Core function replicable by platform owner | High. Absorbed or made obsolete within one product cycle |

| Certified compliance tooling | Moderate. Regulatory relationships and certifications create stickiness | Medium. Valuable to acquirers but replaceable over time |

| Biometric hardware with on-device processing | High. Physical form factor and proprietary algorithms resist software substitution | Low to medium. Depends on patent breadth |

Assessing biometric tech for competitive advantage requires examining whether the authentication method is genuinely on-device or whether it routes sensitive biometric data through a cloud API. On-device processing is the defensible architecture. Cloud-dependent biometrics inherit the platform risk of whoever owns the API.

Pro Tip: Map every core function of the product to either a proprietary component or a third-party dependency. If more than 40% of the security logic depends on a vendor the startup does not control, the moat is thinner than the pitch suggests.

How to evaluate financial returns in cybersecurity hardware investments

Financial evaluation of hardware cybersecurity ventures requires understanding both the valuation mechanics and the liquidity dynamics specific to this asset class. Cybersecurity M&A revenue multiples in 2026 range from 4x to 45x ARR, with the spread driven by growth rate, revenue quality, and buyer urgency. A company growing at 80% ARR with multi-year enterprise contracts and SOC2 Type II certification commands a very different multiple than one growing at 20% on month-to-month contracts.

Recurring revenue is the primary valuation driver. Multi-year contracts with government agencies or regulated financial institutions carry a premium because they signal both stickiness and compliance credibility. Concentration risk cuts in the opposite direction. A hardware venture generating 60% of revenue from a single customer is a liability, not an asset, regardless of the contract length.

Key financial metrics to track across the portfolio:

-

TVPI vs. DPI: DPI measures actual realized returns, not paper valuations. Top-quartile funds target 3.0x or higher TVPI with 25% or higher IRR. Median funds deliver 1.5x to 1.8x TVPI with 10 to 14% IRR. Prioritize DPI when evaluating fund managers, because hardware ventures carry longer liquidity timelines than software.

-

Revenue quality: Prioritize annual or multi-year contracts over monthly recurring revenue. Hardware deployments with high switching costs justify longer contract terms.

-

Governance positioning: Ventures with independent board members, clean cap tables, and documented compliance roadmaps attract strategic acquirers. Governance gaps create valuation discounts at exit.

-

Exit pathway clarity: Identify whether the most likely exit is a strategic acquisition by a platform vendor, a private equity rollup, or an IPO. Hardware companies with government contracts often attract defense-focused acquirers willing to pay strategic premiums.

What market trends and biases should investors watch in 2026

The most significant market distortion in hardware cybersecurity today is the systematic underinvestment in on-premises solutions. Nir Zuk, the founder of Palo Alto Networks, launched Cylake with $45 million specifically to address what he identifies as a $100 billion market ignored due to cloud bias. That signal from one of the most credible operators in the industry deserves serious attention.

“Industry overfocus on cloud solutions leaves high-regulated environments poorly served, posing both opportunity and risk for investors willing to look where the consensus is not.” — Market blind spot in on-premises cybersecurity hardware

Herd behavior and recency bias have pushed venture capital toward cloud-native security platforms at the expense of hardware-first solutions serving defense, critical infrastructure, and regulated financial institutions. These segments cannot migrate to cloud architectures due to air-gap requirements, data sovereignty laws, or latency constraints. The deep tech security commercialization path for on-premises hardware is longer, but the competitive density is far lower and the switching costs are structurally higher.

Proof-of-concept contracts with a named government agency or a Tier 1 regulated institution are the most credible signal that a hardware venture has cleared the hardest part of the sales cycle. Investors who require this evidence before committing capital avoid the majority of hardware ventures that stall at procurement.

Key takeaways

Effective cybersecurity hardware venture assessment combines quantitative technical benchmarks with rigorous IP verification, competitive moat analysis, and disciplined financial evaluation to separate defensible opportunities from well-marketed commodities.

| Point | Details |

|---|---|

| Technical benchmarks are non-negotiable | Require greater than 99% detection accuracy, sub-24-hour response, and churn below 8% before advancing any deal. |

| IP ownership determines moat depth | Proprietary cryptographic hardware and patented sensor designs resist commoditization; API wrappers do not. |

| DPI outranks TVPI for hardware funds | Realized cash returns matter more than paper marks given the longer liquidity timelines of hardware ventures. |

| On-premises is the neglected opportunity | Cloud bias has left regulated industries underserved, creating a structural opening for hardware-first security solutions. |

| Compliance is a floor, not a ceiling | SOC2 Type II and NIS2 alignment are baseline requirements; technical defensibility is what drives valuation premiums. |

Why I think most hardware security assessments miss the point

Most investors approach a hardware cybersecurity assessment the same way they would evaluate a SaaS company. They look at ARR growth, NRR, and CAC payback. Those metrics matter, but they miss the variable that actually determines whether a hardware security company survives the next platform consolidation cycle: the depth of its physical and cryptographic IP.

I have seen well-funded ventures with impressive compliance stacks and clean financials get absorbed by a platform vendor within 18 months of a Series B because their core authentication logic ran on a licensed API. The acquirer paid a modest multiple, the founders celebrated, and the product was deprecated within a year. That is not a successful exit. It is a controlled failure with a press release.

The ventures worth backing in 2026 are the ones solving problems that cannot be fixed with a software patch. On-device biometric processing, quantum-resistant cryptographic hardware, and spatial authentication systems built on proprietary sensor arrays are the categories where the moat is physical, not just contractual. These are also the categories where most generalist VCs lack the technical depth to conduct a credible assessment, which is precisely where the opportunity concentrates.

Patience matters here too. Hardware security ventures have longer development cycles, longer sales cycles, and longer paths to liquidity than software. Investors who size positions accordingly and maintain dry powder for follow-on rounds are the ones who capture the full return. Chasing a quick exit in this category is how you end up with a 1.2x DPI and a story about the one that got away.

— Joshua

How Jett Optics approaches hardware security assessment

Jett Optics builds the category of hardware security that passes the most demanding venture assessment criteria: proprietary cryptographic architecture, on-device biometric processing, and quantum-resistant encryption that does not depend on any third-party API for its core security function. The optical spatial encryption platform at Jett Optics uses AGT gaze tensors and spatial authentication to convert human biometric inputs into cryptographic keys, creating a physical moat that platform consolidation cannot replicate. For investors and operators evaluating where hardware security is heading in 2026, Jett Optics’ work on DePIN-compatible authentication and encrypted messaging via JettChat represents the architecture that the next generation of secure environments will require.

FAQ

What is cybersecurity hardware venture assessment?

Cybersecurity hardware venture assessment is the structured evaluation of hardware security startups using technical, market, and financial due diligence to determine investment viability. It differs from software venture assessment by requiring physical IP verification, supply chain analysis, and hardware-specific deployment benchmarks.

What threat detection rate should a hardware security startup achieve?

Top-performing hardware cybersecurity ventures achieve greater than 99% threat detection accuracy with a false positive rate below 0.1%. Mean time to incident response should fall under 24 hours, compared to the industry average of 197 days.

Why does DPI matter more than TVPI in cybersecurity hardware funds?

DPI measures actual cash returned to investors, while TVPI includes unrealized paper valuations. Hardware ventures have longer liquidity timelines than software, so DPI provides a more accurate picture of real fund performance.

What are the biggest red flags in a hardware cybersecurity startup?

The absence of a bug bounty program, reliance on third-party APIs for core security functions, and lack of SOC2 Type II certification are the three most common disqualifying signals. A founding team with no prior hardware security experience compounds each of these risks.

How do valuation multiples work for cybersecurity hardware acquisitions?

Cybersecurity M&A multiples in 2026 range from 4x to 45x ARR depending on growth rate, revenue quality, and buyer urgency. Ventures with multi-year government contracts, proprietary IP, and strong compliance posture command the upper end of that range.