TL;DR:

- Cybersecurity deeptech investments in 2026 focus on categories like AI-native SecOps, post-quantum cryptography, zero trust architecture, and advanced identity frameworks. Investors demand measurable outcomes such as operational cost reductions, investigation throughput, and contractual performance commitments to evaluate promising companies effectively. These interconnected categories address foundational security gaps and are driven by regulatory standards, enterprise needs, and technological innovation.

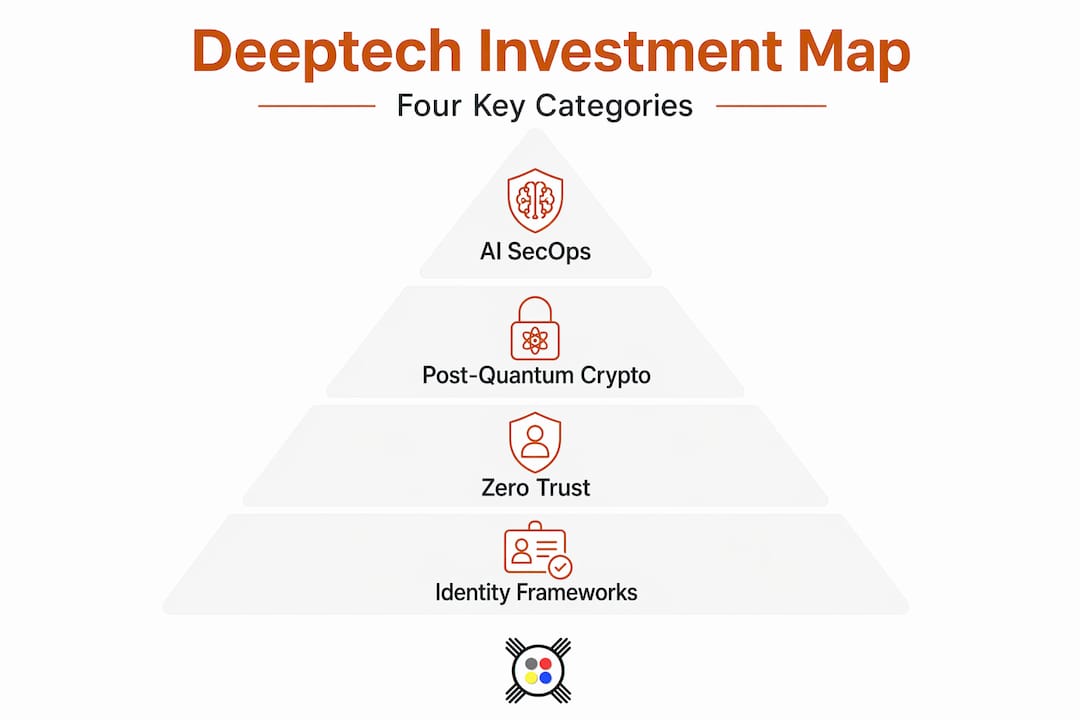

The cybersecurity deeptech investment categories drawing serious capital in 2026 look nothing like they did three years ago. Investors who previously funded broad AI security platforms are now demanding proof of operational cost reduction, measurable risk outcomes, and defensible technical differentiation. The informal phrase "deeptech investments" maps closely to what the industry formally calls deep technology ventures: companies whose competitive moat derives from foundational scientific or engineering breakthroughs rather than business model innovation alone. This guide breaks down the four primary categories attracting institutional capital right now: AI-native security operations, post-quantum cryptography, zero trust architecture, and next-generation identity frameworks.

Table of Contents

- Key Takeaways

- Cybersecurity deeptech investment categories: the 2026 map

- What investors actually want in AI cybersecurity in 2026

- Post-quantum cryptography: where the migration investment goes

- Zero trust architecture as an investable category

- Emerging identity frameworks for AI agents and non-human entities

- My perspective on evaluating these categories

- Jett Optics and the applied side of these investment themes

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| AI-native SecOps attracts capital | Platforms automating alert investigation and reducing analyst workload deliver measurable ROI that investors now demand. |

| PQC migration is a multi-workstream problem | Successful investments address key management, protocol updates, and interoperability, not just algorithm replacement. |

| CISA's five-pillar model is your underwriting lens | Map startup capabilities to Identity, Devices, Networks, Applications, and Data pillars to gauge real maturity. |

| Identity control planes are expanding | Modern identity frameworks must handle AI agents and non-human entities, not just human users with passwords. |

| Outcome evidence wins funding | 71% of investors expect decisive ROI within three years, making contractual performance commitments a strong signal. |

Cybersecurity deeptech investment categories: the 2026 map

Before allocating capital, you need a clear taxonomy. The four primary investment categories in cybersecurity deeptech each carry distinct technical risk profiles, regulatory tailwinds, and time-to-revenue horizons.

| Category | Core Technical Claim | Key Risk Factor |

|---|---|---|

| AI-native SecOps | Autonomous alert triage and investigation | Proof of coverage SLA enforcement |

| Post-quantum cryptography | Quantum-resistant algorithm integration | Migration complexity across stacks |

| Zero trust architecture | Continuous verification across all pillars | Vendor fragmentation and pillar gaps |

| Next-gen identity frameworks | Agent-aware authorization control planes | Interoperability with legacy IAM systems |

Each category represents a distinct thesis. AI-native security operations platforms focus on automating detection, investigation, and response workflows that currently consume most of an analyst's time. Post-quantum cryptography (PQC) addresses the impending cryptographic obsolescence of RSA and ECC-based systems. Zero trust architecture investment funds the enforcement infrastructure that replaces perimeter-based access models. Next-generation identity frameworks extend authorization logic to cover AI agents, service accounts, and non-human entities that existing IAM systems were never designed to handle.

The critical point for investors is that these categories are architecturally interdependent. Zero trust treats identity as its primary control-plane dependency. PQC migration affects every protocol endpoint that zero trust enforces. AI-native SecOps monitors the behavioral signals that zero trust verification generates. Understanding the category map is the prerequisite for evaluating any individual company.

- AI-native SecOps: Covers platforms that replace legacy SIEM-plus-analyst workflows with autonomous investigation pipelines, agentic triage engines, and organization-level security posture reporting.

- Post-quantum cryptography: Encompasses algorithm libraries, crypto-agility frameworks, key management migration tooling, and protocol-level integration services.

- Zero trust architecture: Spans identity enforcement, device trust attestation, network micro-segmentation, application access control, and data classification systems.

- Next-gen identity: Includes dynamic authorization engines, scoped token issuance for AI agents, decentralized identity protocols, and continuous verification platforms.

You can explore the deeptech commercialization path across these categories to understand how startups in each move from lab-stage technology to revenue-generating products.

What investors actually want in AI cybersecurity in 2026

The headline number is significant but incomplete. 80% of cybersecurity investors plan to increase AI cybersecurity funding in 2026, with 42% citing cost reduction as their primary driver. But the shift in evaluation criteria is what matters more than the funding volume itself.

The AI wrapper problem is real and well-documented. 54% of investors say AI wrappers over legacy tools disappointed, and 52% actively screen them out of consideration. The distinction between a true AI-native platform and a GPT interface bolted onto an existing SIEM is technical, not cosmetic. Investors with domain knowledge are now asking specific architectural questions:

- Does the platform perform autonomous investigation, or does it surface recommendations for analysts to act on?

- Can the company demonstrate cost reduction per incident investigated, not just alert volume processed?

- Does the product integrate atop existing SIEM/XDR infrastructure, or require full replacement? Startups that commit to investigational coverage SLAs while layering over existing tooling achieve a defensible market position.

- Is there contractual accountability for performance outcomes?

The Qevlar AI example is instructive. Qevlar AI raised $30M in March 2026 specifically because it demonstrated autonomous alert investigation at scale, reducing investigation costs by a factor of ten. The funding thesis was not "AI in cybersecurity" broadly. It was a specific, measurable claim about investigation throughput and analyst leverage.

Pro Tip: Ask every AI SecOps company you evaluate to show you their investigation closure rate per analyst per shift before and after deployment. If they cannot produce that number, the product is still in the alert-surfacing category, not the autonomous-investigation category.

Cybersecurity venture returns in AI SecOps are increasingly tied to whether platforms can deliver that specific operational outcome at a cost structure that makes sense for mid-market and enterprise buyers alike.

Post-quantum cryptography: where the migration investment goes

The PQC investment thesis begins with a regulatory forcing function. NIST finalized FIPS 203, FIPS 204, and FIPS 205 in August 2024, giving enterprise and government procurement teams the baseline they needed to begin formal migration planning. That planning phase is now converting into procurement dollars, and the investment opportunity is larger than most analysts initially sized.

The mistake many investors make is treating PQC as a pure cryptography play. The actual market is in migration infrastructure. PQC migration costs span multiple workstreams beyond swapping algorithm implementations:

- Key management migration: Existing HSMs, key rotation policies, and lifecycle management systems require updates or replacement to support PQC key material.

- Protocol endpoint updates: TLS, SSH, and S/MIME endpoints across the stack must be updated, each with its own testing and validation surface.

- Interoperability testing: Hybrid classical/PQC operation during the transition window requires careful protocol negotiation to avoid downgrade attacks.

- Crypto agility frameworks: Organizations need the ability to swap algorithms without rearchitecting applications, which is a software engineering discipline in itself.

| PQC Investment Sub-category | Maturity Stage | Investor Attraction |

|---|---|---|

| Algorithm library providers | Mature | Low differentiation, commoditizing |

| Crypto agility middleware | Growth | High demand, sticky integration |

| Key management migration tooling | Early growth | Clear ROI, regulatory pull |

| Protocol validation and testing | Nascent | Specialized, limited competition |

Startups that reduce migration risk and shrink the operational surface area of the transition attract the strongest interest. The $15 billion PQC migration market is not a single procurement event. It is a multi-year, multi-workstream program that creates recurring revenue opportunities for integration-layer companies. You can review encryption venture categories to map the full spectrum of companies operating in this space.

Pro Tip: When evaluating a PQC startup, request a migration cost model that breaks down key management, protocol, and interoperability workstreams separately. A founder who cannot produce that breakdown has likely not engaged with enterprise procurement teams yet.

Zero trust architecture as an investable category

Zero trust is not a product. It is an architecture, which means the investment category is defined by the companies that build the enforcement infrastructure to implement that architecture. The CISA Zero Trust Maturity Model v2.0 provides the most practical framework available for mapping startup capabilities to measurable security outcomes.

The model organizes zero trust across five pillars, each with four maturity levels:

- Identity: Authentication, authorization, and credential management for all users and entities.

- Devices: Trust attestation, compliance verification, and endpoint behavior monitoring.

- Networks: Micro-segmentation, encrypted traffic inspection, and access control enforcement.

- Applications: Workload isolation, API security, and least-privilege access to application resources.

- Data: Classification, labeling, access governance, and data-level encryption enforcement.

Maturity levels progress from Traditional (perimeter-based, manual processes) through Initial (partial automation, limited telemetry) and Advanced (integrated policies, machine-assisted verification) to Optimal (fully automated, continuous verification with dynamic policy enforcement).

The practical value of this framework for investors is that it converts vendor claims into falsifiable questions. Zero trust investments that map directly to maturity model enforcement points and deliver measurable pillar progression outperform those evaluated on feature checklists alone. Most enterprise buyers have uneven maturity across pillars, which means targeted, pillar-specific solutions with clear upgrade paths attract predictable budget.

Enterprise security scalability examples illustrate how organizations are actually deploying zero trust infrastructure, which is useful context when assessing a startup's go-to-market claims against real procurement patterns.

Also worth noting: 66% of cyber risk leaders globally plan to increase cybersecurity spending with a focus on cyber resilience, not just breach prevention. Zero trust architecture sits directly in that budget line because it addresses both breach containment and audit compliance simultaneously.

Emerging identity frameworks for AI agents and non-human entities

Traditional IAM was built for humans logging into applications. That mental model is now a liability. Modern enterprise environments include service accounts, API integrations, container workloads, robotic process automation bots, and increasingly, autonomous AI agents making real-time decisions on behalf of organizations. Each of these entities needs identity, authorization, and verification treatment that legacy IAM systems cannot provide.

The investment thesis in next-generation identity frameworks centers on three specific technical capabilities:

- Scoped, time-limited tokens: Rather than granting persistent permissions, modern identity systems issue tokens with explicit scope boundaries and expiration windows. This limits the blast radius when a service account or AI agent is compromised.

- Continuous verification models: Authorization is not a one-time check at login. It is a persistent evaluation of behavior, context, and risk signals that can revoke or modify permissions in real time.

- Agent-aware control planes: Identity serves as a control-plane dependency in modern zero trust architecture, and extending that control plane to cover AI agents requires fundamentally different authorization logic than human user management.

The decentralized identity startups entering this space are pursuing on-chain credential verification, self-sovereign identity models, and cryptographic attestation that can operate across organizational boundaries without centralized identity providers. For investors, the key differentiator is whether a startup's identity model can handle non-human principals at the protocol level, not just through policy overlays applied after the fact.

The convergence of zero trust architecture with agent-based AI deployment is creating a category of identity infrastructure that did not exist three years ago. Startups building authorization engines capable of managing dynamic permissions for AI agents operating across hybrid and decentralized environments are addressing a genuine technical gap, and the timing aligns with enterprise AI deployment schedules.

My perspective on evaluating these categories

I've spent considerable time stress-testing investment theses across these four categories, and the pattern that consistently separates strong bets from promising-sounding ones is outcome specificity.

In AI SecOps, the true differentiator is not the AI architecture itself. It's whether the company has a contractual performance commitment attached to investigation outcomes. Any team can demo impressive alert correlation. Far fewer can show you a signed enterprise contract with SLA penalties tied to investigation closure rates.

For PQC, the long-term nature of the migration thesis is something many investors underestimate. This is not a two-year deployment cycle. Enterprise PQC migration programs will run five to ten years, and the companies that will generate sustained revenue are the ones building migration orchestration platforms with multi-workstream cost visibility, not just libraries implementing CRYSTALS-Kyber or CRYSTALS-Dilithium.

Using CISA's zero trust maturity model as an underwriting framework is something I'd recommend to any analyst evaluating this space. The model gives you a vendor-neutral vocabulary to challenge claims and map capabilities to documented maturity gaps.

What most investors miss about identity innovation is its architectural centrality. When identity fails, everything else fails with it. Companies that get agent-aware authorization right early will have structural advantages as AI deployment accelerates across enterprise environments. The common due diligence mistakes in this space almost always involve treating identity as a feature rather than a foundational infrastructure category.

Balancing optimism with rigor is not a soft skill here. It is the core competency.

— Joshua

Jett Optics and the applied side of these investment themes

The investment categories described throughout this article are not abstract. They have real product expressions, and Jett Optics represents one of the most technically differentiated examples of applied deeptech across zero trust identity, PQC, and spatial authentication simultaneously.

Jett Optics builds spatial encryption and biometric authentication systems that treat human gaze as a cryptographic key, combining AGT gaze tensors with quantum-resistant encryption and DePIN-compatible on-chain verification. JettChat encrypted messaging applies spatial encryption to secure communications, directly instantiating the zero trust identity pillar through continuous biometric verification rather than static credentials. Jett Optics' post-quantum spatial encryption platform addresses the PQC migration category at the authentication layer, where most enterprise migration programs begin. For investors mapping deeptech exposure across the categories covered here, Jett Optics' architecture spans multiple pillars in a single integrated system.

FAQ

What are the main cybersecurity deeptech investment categories in 2026?

The four primary categories are AI-native security operations, post-quantum cryptography, zero trust architecture, and next-generation identity frameworks. Each addresses a distinct technical gap with measurable enterprise demand and regulatory tailwinds.

How do investors evaluate AI cybersecurity companies beyond hype?

Investors now require evidence of operational cost reduction and investigation throughput improvements within three years, with 71% expecting decisive ROI evidence by that deadline. Companies that automate SecOps outcomes rather than augmenting analyst workflows attract stronger interest.

What makes post-quantum cryptography a viable deeptech investment?

PQC migration spans key management, protocol updates, interoperability testing, and crypto agility, not just algorithm replacement. The multi-workstream cost structure creates durable revenue opportunities for integration-layer startups serving enterprise programs that will run for years.

How should investors use the CISA zero trust maturity model?

Map a startup's product capabilities directly to the five pillars (Identity, Devices, Networks, Applications, Data) and four maturity levels to identify whether it delivers measurable pillar progression or only feature-level improvements. This approach converts vendor claims into falsifiable technical assessments.

Why does identity matter so much across all four investment categories?

Identity functions as the control-plane dependency across zero trust, AI SecOps, and PQC implementations. Systems that cannot handle AI agents and non-human entities with scoped, time-limited tokens represent architectural debt that will require replacement as enterprise AI deployment accelerates.