TL;DR:

Google’s $32 billion acquisition of Wiz in 2025 significantly elevated cybersecurity venture returns and market expectations.

Investor success depends on understanding fund-level metrics, valuation drivers, and strategic buyer pricing mechanics beyond just deal flow.

When Google’s $32 billion acquisition of Wiz closed in 2025, it didn’t just make headlines. It rewrote the perceived ceiling for cybersecurity venture returns. Yet most investors still approach this sector without a clear framework for evaluating what separates a 17x multiple from a fund that barely returns capital. Cybersecurity venture returns explained properly require more than tracking deal flow. They demand fluency in fund-level metrics, valuation drivers, and the mechanics of how strategic acquirers actually price security assets. This article provides that framework, grounded in current market data.

Table of Contents

Key Takeaways

| Point | Details |

|---|---|

| Funding surge is real | Cybersecurity venture funding hit $20.7B across 820 deals in 2025, up 52% from 2024. |

| Returns concentrate among winners | Capital concentration in fewer than 100 deals creates extreme return dispersion across fund portfolios. |

| Multiples vary dramatically | Cybersecurity M&A revenue multiples range from 10x to 45x depending on growth rate and strategic fit. |

| Partial exits generate real returns | Partial liquidity events can deliver significant DPI before a full exit, as seen in the CloudSEK case. |

| Strategic buyers dominate | Strategic acquirers drove 92% of M&A capital in 2025, making buyer fit a core variable in return modeling. |

Venture funding trends shaping today’s returns

The capital environment for cybersecurity has shifted considerably. Cybersecurity venture funding totaled $20.7B across 820 deals in 2025, representing a 52% increase over 2024. Median Series C+ deal sizes exceeded $80 million, a figure that reflects how quickly the market has moved toward backing scale-ready businesses rather than early-stage experiments.

Several structural dynamics are reshaping how returns get generated:

-

Capital concentration: Fewer than 100 deals attracted over $34 billion in Q4 2025 alone, creating a two-tiered market where a small number of high-growth companies absorb most institutional capital.

-

Platform consolidation: Strategic acquirers are actively buying to build platforms rather than acquire point solutions. This behavior compresses the time between late-stage funding and exit, which directly benefits venture investors holding later-round positions.

-

M&A volume and scale: 426 cybersecurity M&A deals were announced in 2025, totaling $92.5 billion in disclosed value. Eleven of those deals exceeded $1 billion individually.

-

IPO market reopening: After years of constrained public market exits, signs of renewed IPO activity offer venture funds an alternative path to liquidity beyond trade sales.

Pro Tip: Pay close attention to how a fund’s vintage year aligns with M&A cycle peaks. Funds deployed in 2021 to 2022 are now reaching natural exit windows precisely when strategic buyer appetite is at its highest.

The concentration of capital isn’t a sign of a healthy broad market. It’s a signal that fund managers with access to the top tier of deals will produce dramatically different outcomes than those without it. For financial analysts evaluating fund managers, this distinction matters more than any macro trend.

Cybersecurity venture return metrics explained

Understanding how venture returns are actually measured separates informed investors from those who mistake paper value for realized performance. Four metrics form the foundation of any credible cybersecurity investment analysis.

Core VC fund metrics

| Metric | Definition | What it tells you |

|---|---|---|

| TVPI (Total Value to Paid-In) | Total value (realized + unrealized) divided by capital invested | Overall fund return including paper gains |

| DPI (Distributions to Paid-In) | Cash distributions divided by capital invested | Actual realized returns delivered to LPs |

| MOIC (Multiple on Invested Capital) | Total exit value divided by cost basis | Return multiple on individual investments |

| IRR (Internal Rate of Return) | Annualized return accounting for time | Time-weighted performance measure |

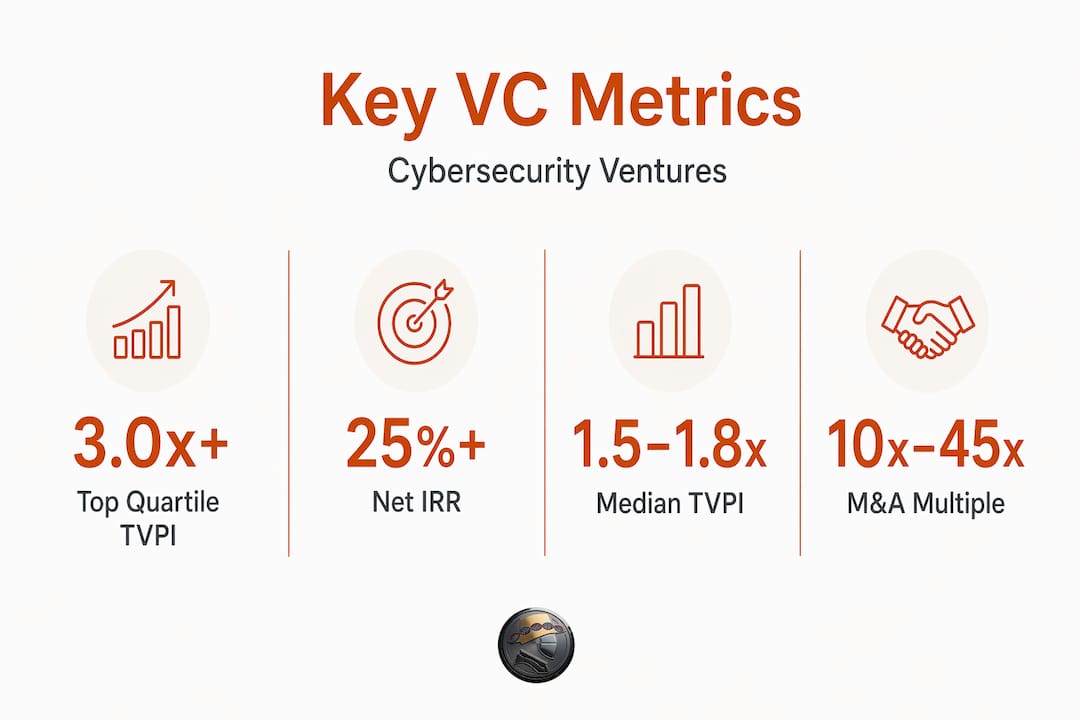

Top-quartile VC funds achieve 3.0x+ TVPI and 25%+ net IRR, while median funds tend to land in the 1.5x to 1.8x TVPI range with 10 to 14% IRR. The cybersecurity sector, given its concentration of outsized exits, skews strongly toward top-quartile performance for the right portfolios.

The most important distinction for institutional investors is the gap between TVPI and DPI. Cybersecurity investments often require years to convert paper value into cash distributions. A fund showing a 4.0x TVPI is not the same as one showing a 2.5x DPI. When evaluating fund managers, prioritize those with demonstrated DPI, not just compelling paper multiples.

On the company level, cybersecurity M&A revenue multiples range from roughly 10x to 45x, depending on growth rate, revenue quality, and buyer urgency. A company growing at 30% annually with 80% recurring revenue from enterprise contracts commands a dramatically different multiple than a slower-growing peer with transactional revenue.

Pro Tip: When modeling a potential exit, build three scenarios around buyer type: a financial buyer (private equity), a strategic platform acquirer, and a public market listing. Each buyer type applies different multiple frameworks, and the range can easily span 15x to 40x for the same business.

Understanding these nuances is critical when assessing biometric tech or any specialized security category where recurring revenue characteristics vary widely from traditional SaaS benchmarks.

Case studies: landmark exits and what they reveal

Abstract metrics only tell part of the story. The real mechanics of cybersecurity venture returns become clear when examined through specific transactions.

The Wiz acquisition is the most significant data point of the decade. Index Ventures turned $245 million invested into $4.3 billion, a MOIC of approximately 17.6x. That return was driven by Wiz’s extraordinary revenue growth trajectory, its broad platform appeal, and Google’s strategic urgency to close a competitive capability gap in cloud security. The deal also illustrates how late-stage funding rounds affect return potential: investors who entered at a $10 billion valuation in earlier rounds captured far more upside than those who committed capital at the $12 billion round just before the acquisition.

The CloudSEK case offers an equally instructive lesson, though at a different scale. Key takeaways from Exfinity Ventures’ exit demonstrate how partial liquidity events work in practice:

-

Exfinity Ventures entered CloudSEK early, during a period when AI-driven threat intelligence was still an emerging category rather than a defined market segment.

-

Rather than waiting for a full exit, Exfinity secured a partial exit delivering 13x MOIC and IRR above 40% while retaining meaningful ownership.

-

The firm’s continued ownership position means additional upside remains available if CloudSEK pursues a larger acquisition or public offering.

-

The partial exit generated DPI for Exfinity’s LPs, demonstrating realized return generation without requiring a full liquidity event.

“Partial and secondary liquidity events can generate meaningful ongoing returns for venture investors, smoothing the traditional binary nature of exits.” — Deep knowledge synthesis from the Exfinity/CloudSEK transaction

This two-part structure, realizing gains while maintaining upside, is a model that sophisticated cybersecurity investors should explicitly seek when evaluating fund managers. Binary all-or-nothing exit structures are increasingly rare in a market where strategic acquirers negotiate partial purchases and secondary markets for LP interests have matured.

Factors that create return variability

Not all cybersecurity funds perform alike, and the gap between top and bottom performers in this sector is wider than in almost any other technology vertical. Understanding why requires examining the specific factors that create return variability.

-

Growth rate premium: Higher growth rates translate nonlinearly into valuation multiples. A company growing at 60% annually may command twice the revenue multiple of a company growing at 30%, even with identical revenue base. Buyers price growth expectations into acquisitions aggressively.

-

Cyber resilience as a differentiator: Cyber attacks can erase a year’s operating profit rapidly, meaning companies that can demonstrate genuine resilience and governance command premium valuations. This isn’t just a qualitative preference. It directly influences the price a strategic acquirer is willing to pay.

-

Revenue quality signals: Recurring revenue from enterprise contracts, particularly multi-year agreements with high switching costs, signals predictable cash flow to acquirers. This predictability directly supports higher multiples and faster deal closings.

-

Capital concentration risk: The concentration of institutional capital into a narrow group of high-growth companies creates a scenario where fund return outcomes are heavily path-dependent. A single fund with Wiz exposure outperformed dozens of competitors solely on that position.

-

Governance and compliance positioning: Fundraising narratives increasingly emphasize compliance and risk reduction, suggesting that future returns will depend not just on growth but on the durability and governance robustness of the underlying business model.

Pro Tip: When evaluating early-stage cybersecurity startups, score them on five revenue quality dimensions: contract duration, renewal rate, expansion revenue, buyer concentration, and compliance certification level. Companies scoring high across all five are the ones that attract the broadest strategic buyer pool at exit.

Applying these insights to your investment decisions

Translating return data into concrete investment decisions requires a disciplined process that most generalist investors don’t apply specifically enough to the cybersecurity sector. The following framework builds on the metrics, case studies, and structural factors covered above.

-

Model exit scenarios by buyer type. Strategic acquirers accounted for 92% of cybersecurity M&A capital deployed in 2025, favoring businesses with high growth, recurring revenue, and clear integration potential. Build your base case around a strategic acquisition, not a financial buyer.

-

Prioritize DPI over TVPI when selecting fund managers. The distinction between paper returns and realized cash is especially significant in a market where valuations can inflate rapidly and correct just as quickly. Ask fund managers for their DPI by vintage year, not just total portfolio marks.

-

Factor in partial liquidity pathways. Not every return event requires a full exit. Funds that actively pursue secondary sales, partial acquisitions, and LP interest transfers provide better liquidity profiles than those waiting for a binary outcome.

-

Use SEC filings to stress-test risk disclosures. Before committing to any cybersecurity fund or direct investment, review company risk disclosures for systemic cyber exposure, customer concentration, and regulatory headwinds that may compress multiples at exit.

-

Benchmark against top-quartile data. If a fund cannot demonstrate a credible path to 3.0x+ TVPI given its current portfolio, the return profile likely doesn’t justify the illiquidity premium over public market cybersecurity equities.

The biometric security industry landscape in 2026 offers a useful lens for understanding which subsectors within cybersecurity are attracting the highest-quality strategic buyer attention right now.

My perspective on what investors consistently get wrong

I’ve spent considerable time analyzing cybersecurity venture returns across market cycles, and the single most persistent mistake I observe is treating volatility as the primary risk factor. It isn’t. The primary risk is misreading the difference between sector growth and company-specific return drivers.

The Wiz outcome was not representative of the average cybersecurity venture investment. It was the product of exceptional market timing, a product that addressed a genuinely acute pain point for hyperscale cloud buyers, and a competitive dynamic at Google that created urgent buyer need. Investors who model their cybersecurity portfolios around Wiz-like return expectations are making the same error as modeling equity portfolios around single-name outliers.

What I find actually moves the needle is a focus on revenue quality and strategic positioning long before exit conversations begin. The CloudSEK partial exit demonstrates this clearly. Exfinity Ventures didn’t generate a 13x return because they timed the market. They generated it because they identified a company with a durable technical moat and positioned themselves to capture partial liquidity before peak-cycle valuations corrected.

Patient capital with selective fund managers, specifically those with proven DPI across multiple vintages and demonstrated access to top-tier deal flow, consistently outperforms the generalist approach. Governance and compliance positioning within portfolio companies will separate the next generation of high-multiple exits from the median. That’s where I’d focus analytical energy.

— Joshua

How Jett Optics fits into the cybersecurity investment thesis

The return dynamics covered in this article reflect a broader market trend: capital is flowing toward cybersecurity businesses with technically differentiated, defensible positions in high-growth categories. Optical encryption, spatial authentication, and biometric security represent exactly the kind of category where strategic acquirer demand is building.

Jett Optics operates at the frontier of this space, developing AGT gaze tensor cryptography, quantum-resistant encryption, and Web3-compatible biometric authentication systems. The platform exemplifies the revenue quality and technical moat characteristics that sophisticated investors identify as multiple-expansion drivers. Investors and analysts tracking the intersection of deep cryptographic technology and next-generation secure communications can explore Jett Optics’ spatial encryption platform for a direct view into how optical cybersecurity creates durable competitive position. For those focused on encrypted communications specifically, JettChat’s gaze-verified messaging demonstrates the applied product layer of this thesis.

FAQ

What metrics measure cybersecurity venture returns?

TVPI, DPI, MOIC, and IRR are the four core metrics. DPI is the most critical for evaluating realized returns because it measures actual cash distributions, not paper value.

What was the return on the Wiz acquisition?

Index Ventures achieved approximately 17.6x MOIC on the Wiz deal, turning $245 million into $4.3 billion when Google acquired Wiz for $32 billion in 2025.

How are cybersecurity company valuations determined at exit?

Cybersecurity M&A revenue multiples range from 10x to 45x, driven by growth rate, recurring revenue percentage, strategic fit with the acquirer, and buyer urgency in the market.

What is a partial exit in venture capital?

A partial exit occurs when a venture investor sells a portion of their ownership stake, generating realized returns before a full company sale or IPO. Exfinity Ventures achieved a 13x MOIC through a partial exit from CloudSEK while retaining upside in the remaining position.

Why do cybersecurity venture returns vary so widely?

Return dispersion is primarily driven by capital concentration. Fewer than 100 deals attracted over $34 billion in a single quarter of 2025, meaning fund returns depend heavily on whether a portfolio includes the top-performing names in that concentrated group.